Running a business has a significant impact on your life and the lives of those you care about. However, before running a business, you must first learn to start one. In this blog, we have listed the steps to start a business in 2022 with no experience.

If you’ve never done it before, deciding how to establish a business might be a daunting task. These tried-and-true methods for starting a business can help you with everything from researching and confirming your money-making concept to thinking out your delivery plan to finally releasing your product or service, whether it’s your first or tenth.

One of the most exciting and fulfilling experiences you can have is starting a business, but where do you start? You have many options for starting your own business, but before you make any decisions, carefully consider your business idea, how much time you have, and how much money you are willing to invest. We’ve put together a list of eight steps to assist you to succeed while launching a business.

Overnight achievements are frequently reported in the media because they make compelling headlines. They don’t see the years of dreaming, constructing, and positioning that go into a big public launch, so it’s rarely that simple. As a result, try to concentrate on your business journey rather than comparing yourself to others.

Consistency is Essential.

New business owners are prone to relying on their motivation at first, only to become dissatisfied as that motivation fades. This is why it’s critical to develop habits and stick to routines that will keep you going when your drive wanes.

Take the Following Step

Some entrepreneurs jump in blindly without looking and make things up as they go. Then some get stuck in analysis paralysis and never get started. You might be a combination of both; in that case, you’re in the right place. The most excellent method to reach any company or personal goal is to write out all of the steps necessary to get there. Then, in order of importance, put those stages in sequence. Some processes may take only a few minutes, while others may take several hours. The objective is always to move forward.

The majority of business advice urges you to monetize what you enjoy, but overlooks two crucial factors: it must be profitable and you must excel at it. For example, you may enjoy music, but how viable is your company idea if you’re not a terrific performer or songwriter? Perhaps you enjoy manufacturing soap and want to create a soap shop in your tiny town. Still, there are already three nearby—it will be challenging to monopolize the market when you’re producing the same product as the others.

Ask yourself the following questions if you don’t have a clear understanding of what your business will entail:

These questions may help you come up with a business concept. They might assist you in developing an idea if you already have one. Once you’ve come up with an idea, evaluate it to determine whether you’re good at it and if it will be successful.

It would be fantastic if your business idea were an outlier, but if it isn’t, you may instead improve on an existing product.

Most entrepreneurs devote more effort to their products than to researching their competitors. When you seek outside money, a potential lender or partner will want to know what makes you (or your business idea) stand out. If market research suggests that your product or service is oversaturated in your location, consider if you can come up with a new strategy. Consider housekeeping: instead of providing general cleaning services, you might focus on cleaning houses with pets or garage clean-ups.

Primary Research

Primary research is the first stage of any competitive study, and it comprises gathering data directly from potential customers rather than drawing conclusions based on previous data. You may find out what customers desire using questionnaires, surveys, and interviews.

Secondary Research

When conducting secondary research, use existing sources of information, such as census data. Current data can be investigated, collated, and analyzed in various ways to meet your goals, but it won’t be as in-depth as primary research.

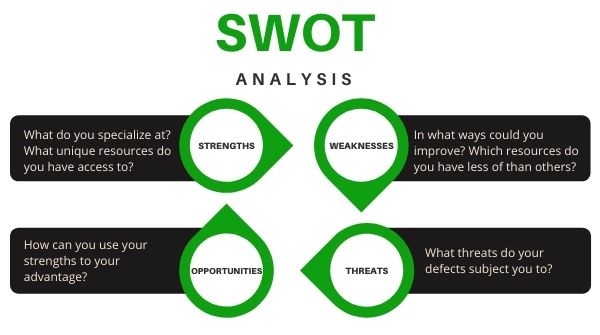

Make SWOT analysis.

SWOT is an acronym for strengths, weaknesses, opportunities, and threats. A SWOT analysis helps you look at the facts about how your product or idea may perform if it were to be put on the market, and it can also assist you in making judgments about where your idea should go.

A business plan is a living document that acts as a road map for starting a new company. This document is easy to grasp and absorb for possible investors, financial institutions, and firm management. Developing a business plan can help you flesh out your concept and identify potential problems, even if you plan to self-fund. The following sections should be included in a well-rounded business plan:

Summary of the report

Although it should be the first item in the business plan, the executive summary should be prepared last. It defines the proposed new business and emphasizes its objectives and techniques for achieving them.

Description of the business

The company description explains how your product or service solves problems and why your company or idea is the best. For example, suppose you have a background in molecular engineering and have used it to develop a new type of athletic clothing. In that case, you have the qualifications to manufacture the most excellent material.

Analyze the market

This business plan component looks at how well a company compares to its competition. Target market, segmentation analysis, market size, growth rate, trends, and a competitive environment evaluation should all be included in the market analysis.

Organization and structure are essential.

Write about the type of company you envision, the risk management measures you offer, and the management team you envision. What are their credentials? Will your company be a sole proprietorship or a corporation?

Mission and objectives

This part should include a brief mission statement that explains what the company wants to achieve and how it plans to get there. These objectives should be SMART (specific, measurable, action-oriented, realistic, and time-bound).

Services or products

This section explains how your company will run. It details what items you’ll give customers at the start of your firm, how they compare to existing competitors, how much your product costs, who will be in charge of creating it, how you’ll acquire resources, and how much they cost to create.

A brief overview of the background

Writing this section of the business strategy takes the most time. Compile and summarize any data, articles, or research papers on trends that could affect your business or sector in a positive or wrong way.

Marketing strategy

The marketing plan describes the features of your product or service, summarizes the SWOT analysis, and examines your competition. It also covers how you’ll market your company, how much money you’ll spend on marketing, and how long the campaign will continue.

Make a budget

The financial strategy is likely an essential part of the business plan because the company will not move forward without money. In your financial plan, including a suggested budget and predicted financial statements such as an income statement, a balance sheet, and a statement of cash flows. Typically, forecasted financial statements for the next five years are acceptable. If you’re looking for outside financing, this is also where you should put your fundraising request.

It’s critical to evaluate how each structure affects the amount of taxes you owe, daily operations, and whether your assets are at risk when establishing your firm.

Limited Liability Corporation (LLC)

A limited accountability company (LLC) protects you from personal liability for commercial debts. Individuals or businesses can own LLCs, and they must have a registered agent. Members are the people who own the property.

Limited Liability Partnership

A limited liability partnership, or LLP, is comparable to an LLC but is reserved for licensed business professionals such as attorneys and accountants. A partnership agreement is required in these situations.

Sole Proprietorship

If you’re starting a solo firm, a sole proprietorship can be a good option. The company and the owner are treated as one entity for legal and tax reasons. The owner assumes the company’s obligation. As a result, if the company fails, the owner is personally and financially liable for all of the company’s debts.

Corporation

Like an LLC, a corporation reduces your accountability for commercial debts. For tax purposes, a corporation can be classified as either a C corporation or an S corporation. Small businesses that meet specific IRS standards can apply for S company status, which allows them to pay taxes at a lower rate. Larger firms, as well as start-ups seeking venture financing, are frequently taxed as C corporations.

Discuss your position with a small business accountant before deciding on a business structure, as each business form has different tax treatments that could affect your bottom line.

After you’ve decided on a business structure, you’ll need to deal with several legal issues. The following is a helpful checklist of things to think about while starting a business:

Choose a name for your company

Make it memorable, but not overly so. If possible, use the same domain name to develop your online presence. A business name cannot be the same as another firm registered in your state, nor can it infringe on a trademark.

Fill out the necessary paperwork with your state to start your business

By completing documents with your state’s business agency–usually the secretary of state–you can officially form a corporation, LLC, or other business entity. You’ll need to designate a registered agent to accept legal documents on your behalf as part of this process. Filing fees are also required. A certificate from the state will be sent to you, which you can use to apply for licenses, a tax ID number, and company bank accounts.

Fill out an application for an Employer Identification Number

A federal employer identification number is required for all firms other than sole proprietorships with no employees. You must file a tax return to the Internal Revenue Service. In most cases, you’ll get your phone number within minutes.

Make an application for the licenses and permits you require

Your industry and jurisdiction decide the legal requirements. To function, most businesses require a combination of local, state, and federal permits. For license information specific to your location, contact your local government agency.

Open a bank account and commercial insurance for your business

Separate your business and personal finances. In the event of property damage, lawsuits, or other issues, you should consider purchasing general liability insurance for your company. Commercial property insurance and product liability insurance may also be advantageous. In most states, workers’ compensation insurance is needed by law if you have employees.

Consider hiring a bookkeeper or investing in accounting software

To handle and track inventory, you’ll need an inventory function in your accounting software if you sell a product. The software should include ledger and journal entries and the capacity to generate financial statements.

There are various ways to fund your business—some involve a significant amount of effort, while others are more straightforward. There are two types of funding: internal and external.

Internal funding consists of the following:

If you finance the firm with your own money or credit cards, you’ll have to pay off the credit card debt, and if the business fails, you’ll lose a significant portion of your wealth. If the company fails, allowing family members or friends to invest in your firm might lead to resentment and broken relationships. External investment may be an option for business owners who seek to reduce these risks.

External sources of funding include:

Small enterprises may need to draw on a variety of funding sources. Consider the amount of money required, the time it will take for the company to repay it, and your risk tolerance—plan for profit regardless of the source you use.

Many entrepreneurs spend so much money developing their goods that they don’t have a marketing budget when they launch. Alternatively, they may have spent so much time producing the product that marketing is a last-minute consideration.

Even if you have a physical location, having a website is necessary. You can create an essential informational website or an e-commerce website to sell things online.

Focus on search engine optimization after creating a website or e-commerce store (SEO). This way, if a potential consumer type in specific terms related to your products, the search engine will direct them to your website. Even if you use all of the proper keywords, SEO is a long-term plan, so don’t expect a lot of traffic from search engines straight away.

Provide high-quality digital information on your website that allows users to locate the solutions to their questions quickly. Videos, client testimonials, blog articles, and demos are good content marketing ideas. Consider content marketing to be one of your most critical daily jobs. This is used in conjunction with social media publishing.

You don’t have to be on every social media platform that exists. You should, however, have a presence on Facebook and Instagram because they both include e-commerce tools that allow you to sell directly from your accounts. Both of these platforms offer free advertising courses to assist you in marketing your company.

Ultrabyte International Pvt. Ltd‘s Marketing services include:

In short, using social media to promote your products and services is more user-friendly and cost-effective. We will renew layouts, improve navigation, and increase conversion rates for a better website strategy. Usually, websites represent your company on the internet. Your digital identity is built on this foundation.